Hi friends!

Although 2020 has been a challenging year for all of us, it has not been without some unexpected benefits. One of them is the new age of virtual employment, which has opened doors for so many to have an opportunity at homeownership. Individuals previously forced to rent in expensive urban areas are now free to move to a larger place, for less money, and have more options. We’re all about that – and Orange County Young Professionals Network is here to support your adventure!

Simple Solutions to Buying, Selling, & Investing in Real Estate

To that end, in 2021 YPN will do our annual Homeownership Day event virtually, and it won’t just be about investing in Southern California real estate. Instead, we’ll be offering local expert agent guidance in many popular cities across the United States, and actually the entire world.

If you haven’t looked at your home as an investment, or considered property as a path toward early retirement, we encourage you to attend the event on January 23, 2021 and look at your real estate in a new light. YES, it’s a place to thrive, to make memories, to customize your taste, to raise your family. But it can be so much more.

You can turn one property into a legacy, and that’s the session I teach & am passionate about. This year’s title is “Concepts to Become An Automatic Millionaire in Southern California & Beyond”; you can register for this 30 minute session by filling out the form below. I’ll educate you on a safe, secure, and timeless strategy for building up your real estate portfolio. These concepts don’t encourage you to stretch yourself too thin, take on a second job, or become a handyman; they are simple and easy to follow. And you can learn them in 30 minutes. I’ll tell you what – if you’ll just commit the time – I’m here to cheerlead you to the finish line.

Owning Property Can Change Your Future

As many of you know, I have been personally working on this strategy for over 15 years now! Because Real Estate is my full time job, we’ve taken it to the next level with vacation rentals, and the creation of Flower Den Retreats. I have found that owning property allows me to truly express myself, whether I’m creating art within, or dreaming up the next concept for a therapeutic space with the ones I love.

I want you to be able to flourish in your space too – are you? If you are, please comment what you love about your home below. Its fun to share our unique ideas 🙂 If you aren’t, fill out the form here and let’s get you on your way in 2021.

If you’re curious to hear what other previous attendees have to say, success stories, or info on the sessions we’ve held in the past, just subscribe to our YouTube Channel. We’ll be uploading new content on the regular. Here’s a video from a couple previous attendees who were able to buy a townhome with barely any money down, and now they are happily raising a family there.

Let Homeownership Day Lead You to Your Happy Place

Sometimes, change is good 🙂 To have a supportive tribe around you as you grow is so helpful, and that’s exactly what you’ll get out of Homeownership Day. Like minded people who want to learn and level up too. All the speakers are no-pressure, happy to answer questions, and excited to connect with you. The vibe of this event will be fresh, fun, educational, and there won’t be a single pitch. Promise. We’ll see you online Jan 23rd!

PS. If you know someone who should be presenting at this event, just connect us by emailing ochomefair@gmail.com & the committee will reach out to them – we love new angles of education and to connect with other professionals across the globe.

Homeownership Day 2021 Sign Up

Did you know 1 in 10 US residents are considering owning international real estate? But how can you protect yourself from making a lemon investment? Thanks to OCR’s Global committee, we have some pointers for you!

Did you know 1 in 10 US residents are considering owning international real estate? But how can you protect yourself from making a lemon investment? Thanks to OCR’s Global committee, we have some pointers for you!  Nicaragua has been a growing spot to get deep discounts in real estate, and Michael personally lived there for 14 years, while raising 2 young daughters. It usually takes about 6-9 months after you visit Nicaragua and sign documents to receive your title, and buying is friendly to foreigners. The country has beautiful scenery, and also offers the following benefits:

Nicaragua has been a growing spot to get deep discounts in real estate, and Michael personally lived there for 14 years, while raising 2 young daughters. It usually takes about 6-9 months after you visit Nicaragua and sign documents to receive your title, and buying is friendly to foreigners. The country has beautiful scenery, and also offers the following benefits: Belize is a tiny country that wasn’t on the radar at all until recently, and now it’s exploding. The title process is 3-6 months, but you can complete a property transaction in just an hour if you’re there in person. English is the official language, so it’s easy to read contracts. Prices are reasonable right now, and the hotspot to check out is Ambergris Caye. Belize was also voted the “most wished for place to visit” on AirBnB, so an excellent consideration for your vacation rental. If you’re thinking of AirBnB, you will have to pay hotel tax, so be sure to factor that in. Speaking of air…air travel has doubled over the last 3 years to Belize, and there is still plenty of room for growth.

Belize is a tiny country that wasn’t on the radar at all until recently, and now it’s exploding. The title process is 3-6 months, but you can complete a property transaction in just an hour if you’re there in person. English is the official language, so it’s easy to read contracts. Prices are reasonable right now, and the hotspot to check out is Ambergris Caye. Belize was also voted the “most wished for place to visit” on AirBnB, so an excellent consideration for your vacation rental. If you’re thinking of AirBnB, you will have to pay hotel tax, so be sure to factor that in. Speaking of air…air travel has doubled over the last 3 years to Belize, and there is still plenty of room for growth.

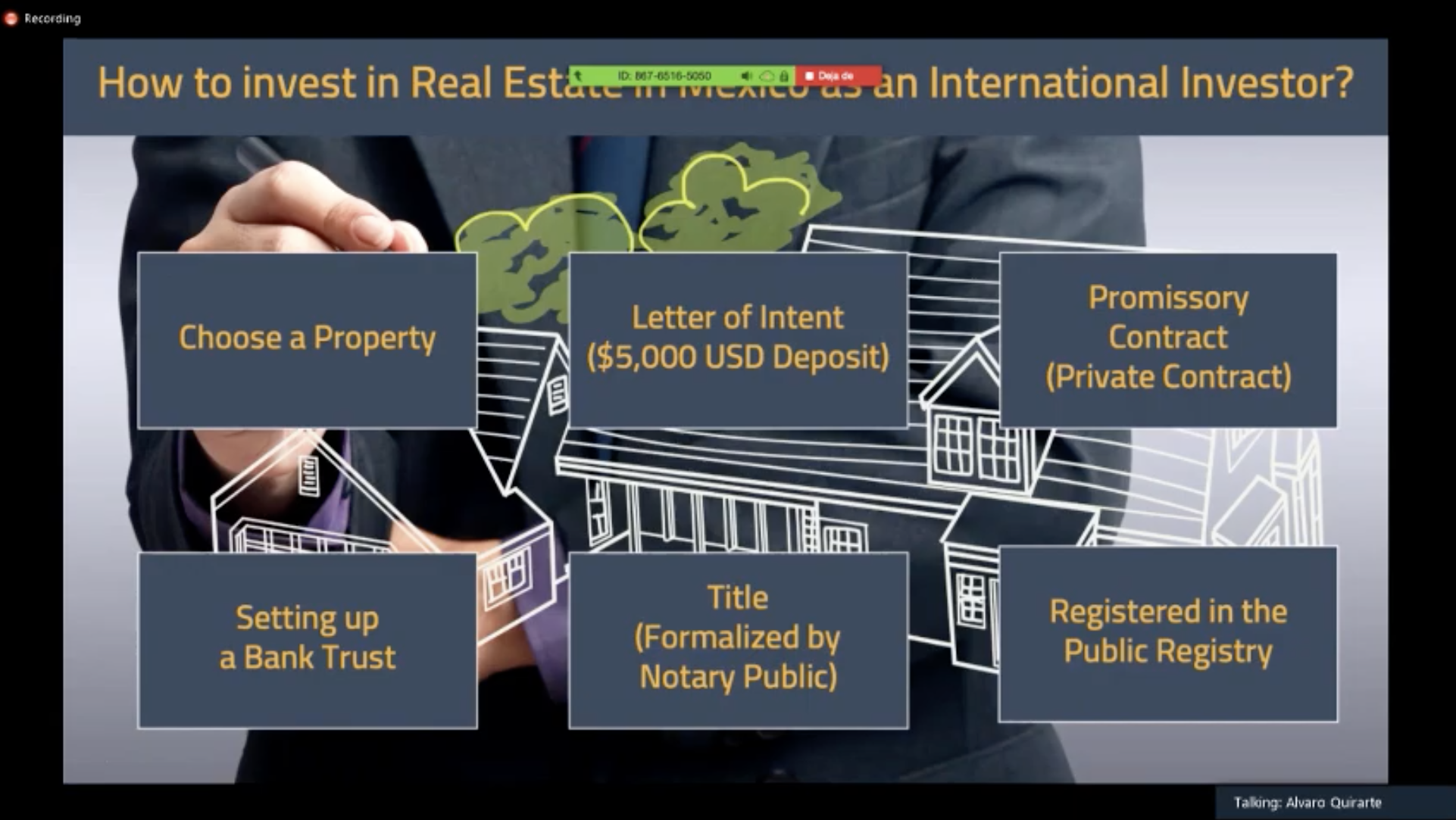

Real Estate expert Alvaro Quirante presented about Riviera Maya and the consistent growth of traffic into the Cancun airport, which creates opportunity. Travel is consistent all year long, so there is no on or off season. Currently they are creating a huge marina, and a theme park, which will create 5000 new jobs in the area. Tulum has been one of the cities that gets the best capital gains each year. A few reasons:

Real Estate expert Alvaro Quirante presented about Riviera Maya and the consistent growth of traffic into the Cancun airport, which creates opportunity. Travel is consistent all year long, so there is no on or off season. Currently they are creating a huge marina, and a theme park, which will create 5000 new jobs in the area. Tulum has been one of the cities that gets the best capital gains each year. A few reasons:

Today we’re spending a Saturday in Pomona at

Today we’re spending a Saturday in Pomona at  These purchase programs (and many others) have some caveats. The home must be your primary residence, and you must pass a homebuyer education class (approx 8 hours). Did you know taking homebuyer education classes before you buy make you 30% less likely to go into foreclosure? This is why many city, bank, and state programs will require you take one before receiving funds. Everyone wants you to succeed in your homeownership venture, so there are milestones like this in place to set you up to win.

These purchase programs (and many others) have some caveats. The home must be your primary residence, and you must pass a homebuyer education class (approx 8 hours). Did you know taking homebuyer education classes before you buy make you 30% less likely to go into foreclosure? This is why many city, bank, and state programs will require you take one before receiving funds. Everyone wants you to succeed in your homeownership venture, so there are milestones like this in place to set you up to win. Union Bank has a 3K down payment assistance grant for closing costs or down payment assistance, which can be layered with other programs. Sorry couldn’t find the link for this exact program, but here are the

Union Bank has a 3K down payment assistance grant for closing costs or down payment assistance, which can be layered with other programs. Sorry couldn’t find the link for this exact program, but here are the

NAWRB supports ALL women as they march to the beat of their own drum. Photo below:

NAWRB supports ALL women as they march to the beat of their own drum. Photo below: